2025/03/18/1842

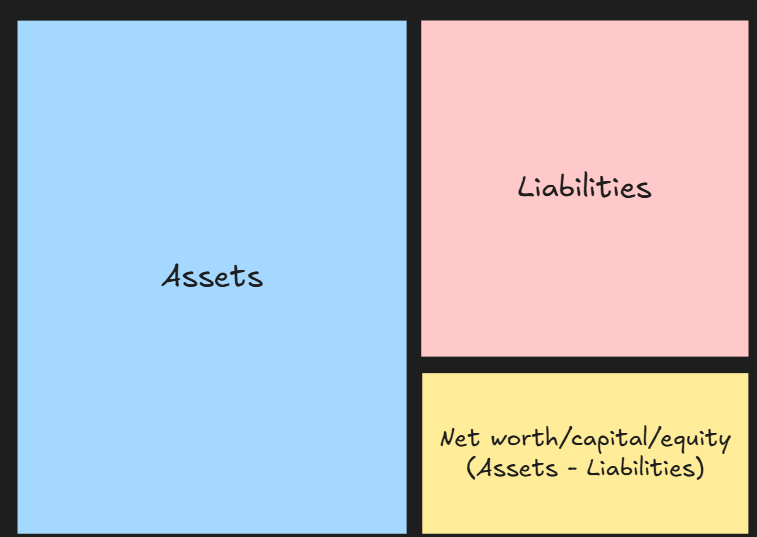

balance sheet

A balance sheet shows the financial position of an economy entity at a particular point of time. It shows the values of stocks of assets and liabilities at start and end of recording period. It comprises both their assets and liabilities. These represent the net (assets-liabilities) financial position of an economic entity, whether it be an individual, firm, or financial institution.

Assets are items of value belonging to the actor in question. Liabilities are (monetary) obligations to make payments to third parties. The excess of value of assets over liabilities is the entities equity (Barker 2011, 20).

Equity = assets - liabilities or Equity = net assets

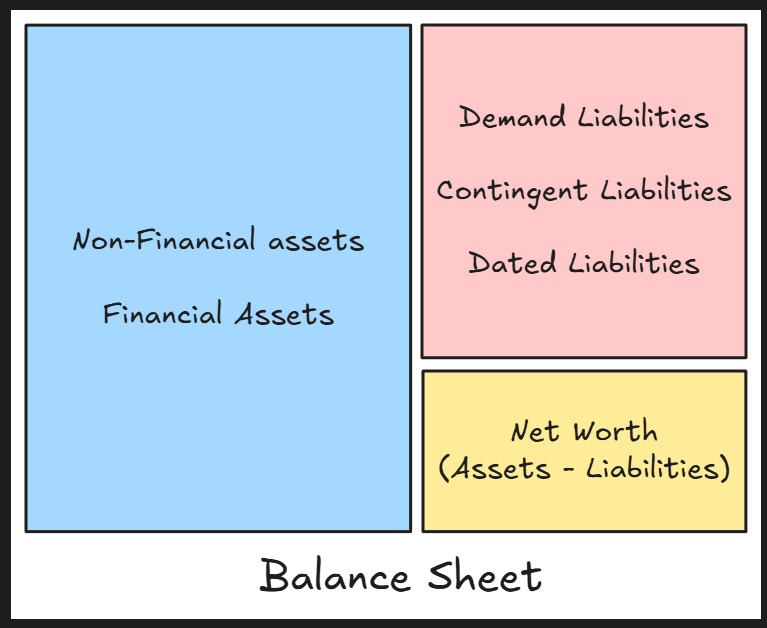

There are a few general categories used to classify both assets and liabilities (Tymoigne, p. 2)

There are two difference ways to classify assets:

Financial Assets: claims on other economic units

Non-Financial Assets (real assets): use-values that are both physical (cars, buildings, machines, pens, desks, inventories, etc.) and intangible (IP, goodwill, brand)

There are three different ways to clasiffy liabilities:

Demand liabilities: those due at the request of creditors (cash withdrawn from a bank account)

contingent liabilities: due when a specific event occurs (life insurance payments, pension payments)

dated liabilities: due at a specific period (interest and principle mortgage payments due every month)

Related

money interest-bearing capital to credit

References

Richard Barker, Short Introduction to Accounting, Dollar ed, Cambridge Short Introductions to Management (Cambridge ; New York: Cambridge University Press, 2011).

Simon M. H. Collin, Dictionary of Accounting, 4th ed (London [Eng.]: A & C Black, 2012).

Tymoigne, Éric. “The Financial System and The Economy.” Textbook. Lewis & Clark College, August 2018.

Planning something?