Why BlackRock's purchase of ports at the Panama Canal is a part of something bigger- The Wall Street Consensus

money-capitals takeover of our infrastructure

A few weeks ago, it was reported that BlackRock, the world's largest asset manager, was going to acquire two major ports along the Panama Canal. The deal is with CK Hutchison, a Hong Kong-based multinational with subsidiaries engaged in infrastructure investment, selling the business to a consortium comprising BlackRock, Global Infrastructure Partners (a BlackRock subsidiary), and Terminal Investment Limited. As part of this 22.8bn deal, the consortium will acquire a 90% stake in a company that owns the two ports: Panama Ports Company (PPC).

PPC currently operates two strategically located ports: Cristobal in the north, and Balboa in the south. The ports will be run on a 25-year concession deal, as all shipping and port infrastructure in the country is overseen Panama Canal Authority, a state-run agency. A concession is a form of contract typically used in different public-private partnerships (P3s). If you haven’t heard of P3s before, it’s one of the most important types of general agreements today between corporations and states.

P3s are defined by the OECD as agreements between government entities and private actors to deliver public goods and/or services in a manner that “the service delivery objectives of the government are aligned with the profit objectives of private partners and where the effectiveness of the alignment depends on a sufficient transfer of risk from the private partner.”1 In practice, the reverse usually happens, and P3s are often about the public sector taking on the risk of project failures, not the private sector. More on that in a second.

Panama has been in the news ever since Trump pressured President Mulino to rescind their involvement in the Chinese Belt and Road project. This is important given that Panama was the first Latin American state to join the BRI. The sale of the port to BlackRock isn't just about economics, as the political pressure from Trump's threats of annexation prompted CK Hutchison to consider the sale:

“When President Trump won and he started making noise about annexing Canada and Greenland and Panama, the pressure was put on the Panamanians,” one person familiar with the deal said. The person added that CK Hutchison “realised that it was a political headache and they wanted to do something.” (Financial Times 2025)

Now, it might not seem to be that big of a deal. Another acquisition by BlackRock, so what? Don’t they own everything already? Funnily enough there was confusion about the deal to the point that Larry Fink himself said when the news broke out, his kids called him asking “BlackRock bought the Panama Canal? Can we go on it?”.

Fink clarified that the deal is about a lot more than just the canal, as they are purchasing about 44 ports around the globe. He also says the deal is another great example of private capital coming in and filling the demand for infrastructure. Ports, according to Fink, are a “great stable business”.

Now, unless you study infrastructure financing, it’s hard to appreciate what is being said here. This isn’t an isolated example of asset managers purchasing infrastructure. Infrastructure has been on the radar of big asset managers over the past two decades. In fact, yesterday in Fink’s annual letter to investors state that the traditional 60/40 portfolio split (between 60% stocks and 40% bonds) “may no longer fully represent true diversification”. Instead, he states:

The future standard portfolio may look more like 50/30/20 — stocks, bonds and private assets like real estate, infrastructure and private credit.

In fact, this isn’t just Fink but other massive investors that are pushing towards a new divide of assets. This 50/30/20 split is actually a lot closer to what many institutional investors are already doing, and while it gives a lot of returns, there are risks from a lack of liquidity.

It’s not easy for most investors to get into infrastructure investment however, as most aren’t publicly offered like shares in companies or bonds on money markets. That’s why BlackRock has been purchasing a lot of private equity companies (Global Infrastructure Partners, Preqin and HPS Investment Partners) to gain access to these markets. Fink mentioned the importance of private market’s in his recent letter to investors:

Most of us associate "markets" with public markets—stocks, bonds, commodities. But you generally cannot buy shares in a new high-speed rail line or a next-generation power grid on the London or New York Stock Exchange. Instead, infrastructure projects are typically investable only through private markets.

Private markets are, as their name suggests, private. For individual investors, they often require higher minimum investments. And even when the minimums are lower, investing is often limited to people with a certain income or net worth.

Nonetheless, there’s a bigger history here with changes in developing financing that combines with the growth of asset managers. The late 1980s to early 1990s was the era of the Washington Consensus (WC), spearheaded by the global north and institutions such as the International Monetary Fund, OECD, World Bank, and so on.

The WC focused on the “Holy Trinity” of market policies, including “macroeconomic stabilization through lower inflation and fiscal discipline; liberalization of trade and capital flows, of domestic product and factor markets; and privatization of state.”2

However, after the repeated crises of the 1990s, including especially the 1997 East Asian crisis, the model began to fall into question. The 2008 financial crisis was the final nail in the coffin, in that it really forced policy makers to rethink their strategy.

The global development policies around infrastructure have consolidated into a model supporting the contemporary power of asset managers. This set of policies, institutions, and practices have been dubbed the Wall Street Consensus (WSC), a term coined by critical finance economist Daniela Gabor. The WSC is pitched as a solution to both the world’s global infrastructure gap and the savings glut through attracting private capital from institutional investors and asset managers to finance infrastructure projects. By the mid-2000s 2000s global development experts began warning of a growing “infrastructure gap”, a disparity between current vs needed infrastructure in particular countries and across the globe.

To combat this, the WSC promotes projects by transforming public infrastructure/services into bankable investments using public-private partnerships (P3s). A fundamental component of making these projects ‘investable’ involves transforming the loans to finance infrastructure into securities of varying risk profiles. The creation of an infrastructure asset class promotes practices of asset-based accumulation and market-based finance. The use of P3s is pushed not only to ‘crowd-in’ private finance, but also to achieve goals such as a green transition and decarbonization, linking it intimately to climate policy as a crucial pillar of its political appeal.

In theory, this investment gap creates the perfect opportunity for institutional investors and asset managers to unload their excess money-capital and resolve the present savings glut they are facing. In practice, to attract private financing, the state must ‘de-risk’ projects to fully, or nearly, guarantee revenue streams for private actors. Asset managers and institutional investors have made it clear that if states want their capital for infrastructure investment projects, they need to ensure that these projects are sufficiently de-risked. This is achieved through policies that, in one way or another, transfer financial risk and responsibility onto the balance sheet of state and/or quasi-state actors.

Even though most people stereotype finance as ‘shortermist’, asset managers are focused on long-term value creation. As BlackRock outlines in a report entitled “The Making of Long-Term Capitalism”, value creation isn’t about the short-term pump and dump of assets. Rather, it’s about finding a source of revenue that will be lucrative for years to come. This is where infrastructure investments come in.

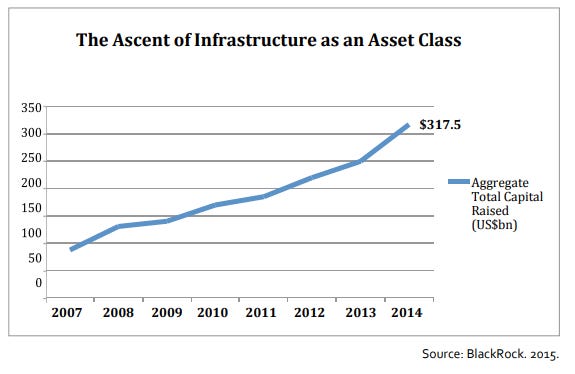

Can you see the connection now? The ongoing deal with BlackRock is merely an extension of these practices. In fact, BlackRock was ahead of the curve, releasing a report as early as 2015 titled “Infrastructure Rising: An Asset Class Takes Shape”, pushing many of the policies that would become central to the WSC.3 In this case, there’s less clear indication of state support from the Panama government. Two lawyers are suing for the contract to be cancelled for the two ports, claiming they are unconstitutional.

Now I actually wrote this piece a few weeks ago but put it to the side, but now, I decided it would be good to publish it given recent updates. It seems China is fighting back against the sale. A few weeks after the initial annoucement, CK got backlash from Ta Kung Pao, a Chinese state-run newspaper in Hong Kong which stated the deal “betrayed and sold out all Chinese people”.

Al Jazeera is stating that Xi was upset because he was hoping the ports would be used as a bargaining chip with Trump. They also report that China is apparently looking to investigate the company for antitrust (hilarious words to use about a ‘socialist’ state) to “protect fair competition in the market and safeguard the public interest”.

The owner of CK Hutchison is 96-year-old billionaire and founder Li Ka-shing. He built his reputation as a businessman navigating the West for the Communist Party. He had a close relationship with Deng, but since the rise of Xi, his influence has waned.

As of April 3rd, the day after Trump’s massive tariff announcement, the deal has been indefinitely delayed. Given all that’s going on Trump hasn’t commented on it yet, but it might come soon. I will keep an eye on this story and continue to post about it in the future. I think sometime next week I will comment on Fink’s letter to investors.

Heather Whiteside, “Public-Private Partnerships: Market Development through Management Reform,” Review of International Political Economy, July 3, 2019, 883, https://doi.org/10.1080/09692290.2019.1635514.

Daniela Gabor, “The Wall Street Consensus,” Development and Change 52, no. 3 (May 2021): 429–59, https://doi.org/10.1111/dech.12645.companies”.

Heather Whiteside, “Austerity Infrastructure Financialization, Offshoring, and Tax Sheltering Public- Private Partnership Funds,” Austerity and Its Alternatives (University of Waterloo, December 2016), https://altausterity.mcmaster.ca/documents/w25-dec-19-2017-heather-whiteside-austerity-infrastructure.pdf.

China nixed that deal.